SpaceX (SPCX) After the Historic IPO: 7 Risks Investors Should Not Ignore

SpaceX’s public-market debut has become one of the biggest investing stories of 2026. The company raised $75 billion in its IPO, priced shares at $135, and surged 19% on its first trading day. After that rally, SpaceX’s market value climbed above $2 trillion, placing it among the world’s most valuable public companies.

The excitement is easy to understand. SpaceX has changed the launch industry with reusable rockets and built Starlink into a global satellite-internet platform. It is also pursuing bigger ambitions, including Starship, artificial intelligence infrastructure, and space-based computing concepts.

But a great company does not automatically make a low-risk stock. After the IPO, investors are no longer judging SpaceX only as a private innovation story. They are now judging it as a public stock with a massive valuation, heavy capital needs, concentrated voting control, and ambitious projects still being proven.

This article focuses on the other side of the SpaceX story. It looks at the risks investors should weigh before assuming the first-day excitement can continue. The goal is not to dismiss SpaceX’s achievements, but to ask a practical question: after such a powerful debut, what could go wrong?

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Always conduct your own research before making investment decisions.

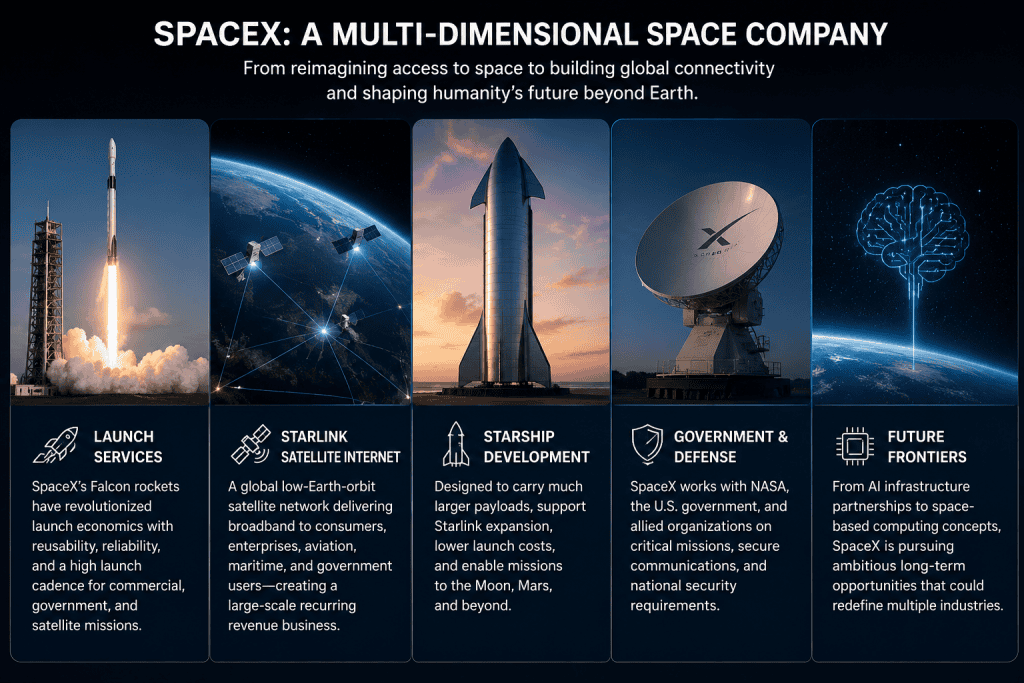

SpaceX Company Overview: More Than a Rocket Company

SpaceX began as a launch company, but investors are now evaluating something much broader. The company sits across launch services, reusable rockets, Starlink satellite internet, Starship development, defense contracts, and newer AI infrastructure ambitions.

The launch business remains the foundation. Falcon rockets helped SpaceX lower launch costs and become a dominant provider for commercial, government, and satellite missions. That launch cadence also gives SpaceX more operating data, stronger customer relationships, and better control over its own satellite deployment schedule.

Starlink is now the company’s most important commercial business. The satellite-internet network gives SpaceX a global recurring-revenue platform that serves consumers, enterprises, aviation, maritime customers, and government users. That is different from launch services, which are more project-based.

Starship is the company’s biggest long-term bet. It is designed to carry larger payloads, support future Starlink expansion, and lower launch costs further. If it scales successfully, Starship could also support Moon, Mars, and space-based infrastructure ambitions.

SpaceX is also pushing beyond rockets and satellites. Its AI-related plans have widened the company’s possible opportunity, but they also make the investment case more complex. Investors are no longer valuing only a launch company; they are valuing a business tied to satellites, rockets, defense, AI infrastructure, and long-term space systems.

Risk #1: A $2 Trillion Valuation Leaves Little Room for Disappointment

The first risk is not that SpaceX is a weak company. The risk is that the stock may already be priced for near-perfect execution.

After its IPO, SpaceX quickly became one of the most valuable public companies in the world. That valuation reflects more than the company’s current launch and satellite-internet businesses. Investors are also paying today for future outcomes tied to Starship, Starlink expansion, artificial intelligence infrastructure, defense contracts, and potentially space-based computing.

That creates a high bar. According to SpaceX’s IPO filing, the company generated approximately $18.7 billion in revenue in 2025, but still reported a net loss of about $4.9 billion. For the first quarter of 2026, SpaceX reported revenue of approximately $4.7 billion, a loss from operations of about $1.9 billion, and adjusted EBITDA of about $1.1 billion.

Those numbers show two things at the same time. SpaceX has real revenue scale, but it is still investing aggressively across several capital-intensive businesses. Launch infrastructure, Starship development, satellite deployment, AI data-center capacity, and global connectivity expansion all require heavy spending before the full financial payoff is visible.

That matters because high-growth stocks can fall even when the company is performing well if expectations move faster than fundamentals. At a multi-trillion-dollar market value, investors are not simply asking whether SpaceX can grow. They are asking whether SpaceX can grow fast enough, profitably enough, and consistently enough to justify one of the largest valuations in the public market.

This does not mean SpaceX is overvalued by default. It means the margin for error is limited. Any slowdown in Starlink growth, delay in Starship commercialization, weaker-than-expected AI returns, regulatory setback, or increase in cash burn could force investors to reassess how much future success should be priced into the stock today.

Risk #2: Starlink Is Strong, but It May Need to Carry Too Much

Starlink is the clearest proof that SpaceX is more than a launch company. The satellite-internet business has real scale, global reach, and a recurring-revenue model that makes it different from the more project-based launch-services business.

According to SpaceX’s IPO filing, the company’s Connectivity segment, which is primarily driven by Starlink, generated approximately $11.4 billion in revenue in 2025. That segment produced about $4.4 billion in income from operations and approximately $7.2 billion in adjusted EBITDA. In the first quarter of 2026, the Connectivity segment generated about $3.3 billion in revenue, $1.2 billion in operating income, and approximately $2.1 billion in adjusted EBITDA.

Those numbers show why investors are excited. Starlink is not just an idea anymore. It is already a large, profitable business and may be the most proven financial engine inside SpaceX today.

The risk is that Starlink may be expected to carry more than its own business. SpaceX is also funding Starship development, launch infrastructure, next-generation satellite deployment, AI infrastructure, orbital-computing ambitions, and other long-term projects. In the first quarter of 2026, SpaceX reported total revenue of approximately $4.7 billion, but still posted a companywide operating loss of about $1.9 billion.

That contrast matters. Starlink may be profitable at the segment level, but SpaceX as a whole is still consuming capital. Investors need to watch whether Starlink’s cash generation can offset the spending required across the rest of the company — especially if AI infrastructure or Starship development takes longer, costs more, or produces revenue later than expected.

The bull case is that Starlink becomes the financial backbone that funds the next stage of SpaceX’s growth. The risk case is that even a strong Starlink business may not be enough if the company’s other ambitions require far more capital than expected.

Risk #3: xAI Adds a New Layer of Financial and Execution Risk

SpaceX’s IPO filing shows that investors are not only buying a rocket, satellite, and launch-services company. They are also buying exposure to artificial intelligence.

In February 2026, SpaceX acquired xAI, the AI company founded in 2023. The filing describes xAI as the first company to build a gigawatt-scale AI training cluster and the “largest coherent supercomputer.” That may expand SpaceX’s long-term opportunity, but it also changes the risk profile of the business.

xAI Is Already a Major Financial Drag

The financial impact is already visible. Reuters reported that SpaceX’s AI division, primarily tied to the xAI acquisition, generated approximately $818 million of revenue in the first quarter of 2026 but accounted for about $2.47 billion of losses. During the same quarter, SpaceX reported a companywide operating loss of approximately $1.94 billion on revenue of about $4.69 billion.

That means xAI is not a small side project. It is a major capital-consuming business inside a company that is already funding Starship development, launch infrastructure, satellite deployment, and global connectivity expansion.

The Strategic Idea Is Big, but Expensive

The strategic idea is easy to understand. SpaceX could combine satellite networks, launch capacity, data-center infrastructure, and AI models into a broader technology platform. Over time, that could create opportunities in AI training, inference, communications, defense, and possibly space-based computing.

The risk is that AI infrastructure is extremely expensive and intensely competitive. SpaceX is entering a field where hyperscalers, chip companies, cloud providers, and AI labs are already spending aggressively. Building large AI data centers requires processors, power, cooling, networking, land, financing, and customer demand strong enough to justify the investment.

There is also a valuation risk. If investors treat xAI as a major future growth engine, SpaceX must eventually show that the AI segment can generate attractive returns on the capital being deployed. High revenue growth alone may not be enough if losses remain large or if AI compute pricing becomes more competitive.

For investors, the key question is not whether AI is a large opportunity. It is whether SpaceX can turn that opportunity into durable profit while also executing on Starlink, Starship, and launch services. The more SpaceX’s valuation depends on AI-related ambitions, the more important xAI’s financial performance becomes.

Risk #4: Starship Is Critical, but Scaling Is Not Guaranteed

Starship is one of the biggest reasons investors assign SpaceX such a large long-term opportunity. The vehicle is designed to carry much larger payloads than Falcon 9, support future Starlink expansion, lower launch costs, and enable longer-term missions to the Moon, Mars, and possibly space-based AI infrastructure.

The opportunity is enormous, but the execution risk is also enormous.

Starship Has Already Consumed Significant Capital

Reuters reported that SpaceX has spent more than $15 billion developing Starship, compared with roughly $400 million spent on Falcon 9. That shows how central the program has become to SpaceX’s future, but also how much capital is tied to making the system work at scale.

Starship has made real progress, including booster recovery milestones, controlled splashdowns, and mock satellite deployment tests. But the program has also experienced explosions, redesigns, launch delays, and regulatory reviews. After the May 2026 Starship Flight 12 test, the FAA required SpaceX to conduct a mishap investigation before further flights could proceed. The FAA said it would oversee the investigation, approve the final report, and review corrective actions before allowing another launch.

SpaceX Needs More Than Test-Flight Progress

The key issue is that SpaceX does not only need Starship to fly. It needs Starship to fly repeatedly, safely, and economically. Many long-term assumptions depend on high launch cadence, reusability, reliable heat shielding, ground infrastructure, and eventually complex capabilities such as in-orbit refueling.

That matters for both Starlink and the broader SpaceX story. Starship is expected to carry larger next-generation Starlink satellites and improve the economics of satellite deployment. It is also tied to NASA’s Artemis lunar-lander plans, Moon and Mars ambitions, and longer-term concepts such as orbital AI compute. If Starship takes longer than expected to scale, several future growth assumptions may be pushed out at the same time.

This does not mean Starship will fail. SpaceX has a history of learning through rapid testing and iteration. But investors should not treat Starship scale as already solved. The gap between a successful test program and a high-cadence commercial launch system remains one of the biggest execution risks in the SpaceX investment case.

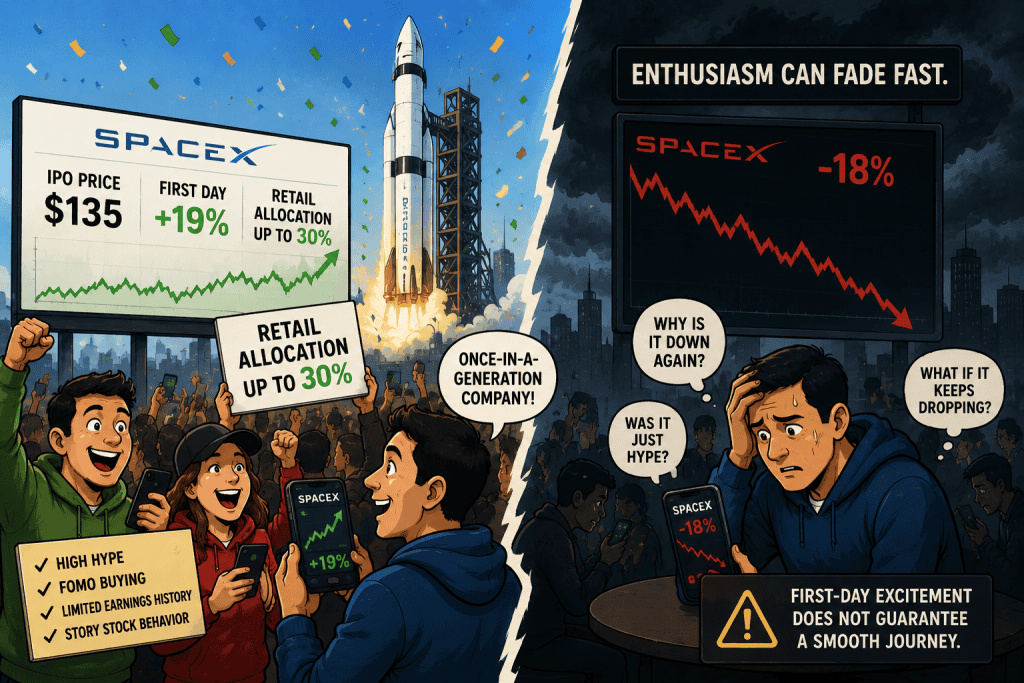

Risk #5: IPO Euphoria Could Create Volatility for Retail Investors

SpaceX’s IPO was not a normal public-market debut. The company raised $75 billion, priced shares at $135, and surged 19% on its first trading day. Reuters reported that SpaceX reserved up to 30% of the IPO allocation for retail investors, far above the typical retail allocation for a major offering.

That retail participation helped make the IPO feel like a public event, not just an institutional transaction. Many individual investors wanted even a small slice of SpaceX because they see the company as a once-in-a-generation business tied to rockets, satellites, Starlink, AI, and Elon Musk’s broader technology vision.

The risk is that story-stock enthusiasm can disconnect price action from fundamentals, at least temporarily. When a company enters the public market with this much attention, early trading can be driven by scarcity, emotion, momentum, and fear of missing out. That can push prices higher quickly, but it can also create sharp downside if sentiment changes.

This matters because SpaceX has limited public trading history and limited public earnings history. Investors do not yet have several quarters of public-company results to judge how the market will react to Starlink growth, Starship progress, xAI losses, regulatory updates, or capital-spending needs.

A successful IPO validates demand for the stock, but it does not guarantee a smooth first year. For retail investors, the main risk is paying a momentum-driven price before the company has had time to prove its public-market earnings pattern.

Risk #6: Future Share Supply Could Pressure the Stock

A separate risk is future share supply.

SpaceX’s first-day trading was supported by enormous demand, but the initial public float represented only a small portion of total shares outstanding. Reuters Breakingviews noted that SpaceX planned to sell less than 5% of its shares in the IPO, compared with an average of nearly 30% for IPOs since 1980.

That limited float can support a strong debut because there are fewer shares available for investors who want exposure. But it can also create a future overhang. Over time, more shares may become eligible for sale as employees, early investors, and other insiders gain liquidity.

SpaceX’s lock-up structure is also different from a simple standard six-month lock-up. Reuters reported that the company planned a phased resale system that could allow a large portion of shares to become eligible for resale before the usual six-month restriction period, depending on company performance milestones. Reuters also reported that SpaceX reserved 5% of IPO shares for certain employees and individuals selected by executive officers, and those reserved shares were exempt from post-IPO lock-up restrictions.

This does not mean insiders are guaranteed to sell aggressively. Many employees and early backers may remain long-term believers in the company. Elon Musk also agreed not to sell stock for about one year after the listing, according to Reuters.

But investors should still monitor share-supply events. A low-float IPO can look very strong at first, but if more shares become available while demand cools, the market may need to absorb that supply at lower prices. For SpaceX, lock-up milestones, reserved-share sales, and future insider liquidity are worth tracking alongside earnings and operating performance.

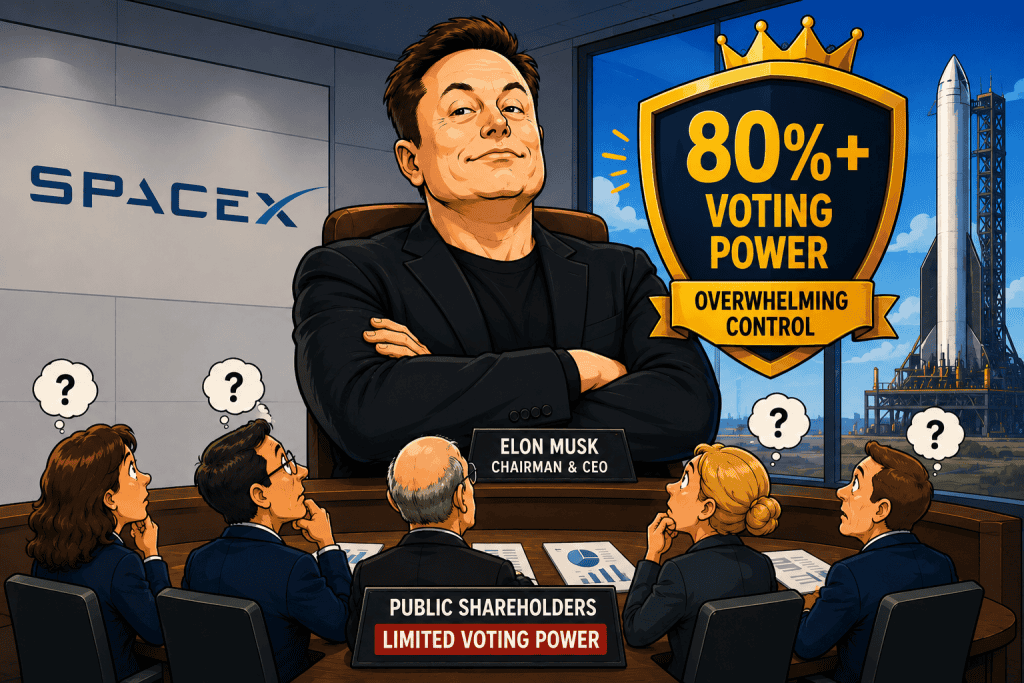

Risk #7: Public Shareholders Have Limited Control

Another risk investors should understand is governance. SpaceX is now a public company, but that does not mean public shareholders have meaningful control over the company’s direction.

SpaceX’s IPO filing shows that Elon Musk will retain majority voting control through the company’s dual-class share structure. Reuters reported that Musk would retain more than 80% of SpaceX’s combined voting power after the IPO. The filing also states that this structure will limit or prevent public shareholders from influencing corporate matters and the election of directors.

That level of control can have advantages. It allows SpaceX to pursue long-term projects such as Starship, Starlink expansion, AI infrastructure, and Mars-related ambitions without being forced to optimize for short-term quarterly results. For a company with extremely long development cycles, that independence may be part of the strategy.

But it also creates risk for public investors. If shareholders disagree with capital allocation, executive compensation, related-party transactions, acquisition decisions, AI spending, or the pace of high-risk projects, they may have little practical ability to change the outcome. Reuters also reported that SpaceX governance provisions could make it difficult to remove Musk as CEO or chairman without his own support.

This means public shareholders are largely along for the ride. They can choose whether to own the stock, but they may have limited influence over how the company is run. That does not make SpaceX uninvestable, but it does mean investors need to be comfortable with a founder-controlled structure where one person’s long-term vision can outweigh the preferences of outside shareholders.

What These Risks Mean for Investors

Taken together, these seven risks do not mean SpaceX is a weak company. They mean the stock is being evaluated against extremely high expectations.

The company has several powerful growth engines: Starlink, launch services, Starship, government contracts, and AI infrastructure. But those same growth engines require major spending, long development timelines, regulatory approvals, and consistent execution. That is why SpaceX can be both one of the most exciting companies in the public market and one of the more difficult stocks to value.

The core investment question is not simply whether SpaceX can grow. The question is whether it can grow fast enough, profitably enough, and predictably enough to justify a valuation already above $2 trillion. At that size, even small disappointments can matter.

Investors should therefore watch a few key signals: Starlink profitability, companywide cash flow, xAI losses, Starship launch cadence, regulatory approvals, future share-supply events, and any updates to Musk’s voting control or governance structure.

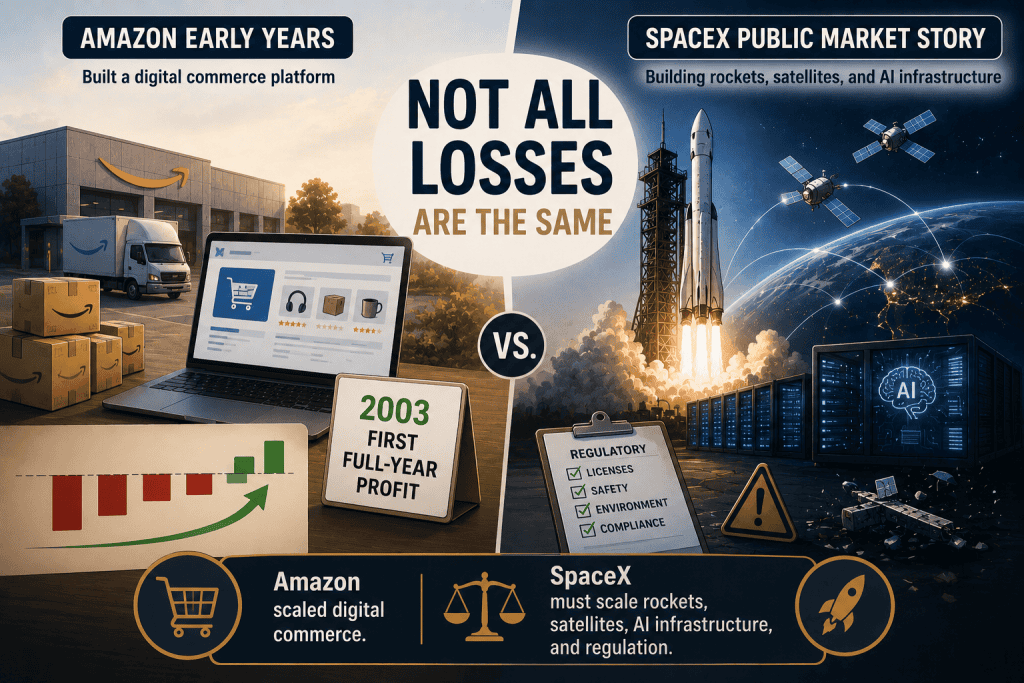

What the Amazon Comparison Gets Right — and What It Misses

Some investors may compare SpaceX to Amazon’s early public-market story. That comparison is not unreasonable. Amazon also spent years prioritizing scale over profits, and the company reported its first full-year profit in 2003, earning $35 million after losing $149 million in 2002. The lesson is that early losses are not automatically a red flag when a company is building a massive long-term platform.

But the comparison has limits. Amazon’s early losses were tied mostly to scaling an internet retail, logistics, marketplace, and eventually cloud platform. SpaceX is scaling businesses that depend on rockets, satellites, launch sites, spectrum rights, regulatory approvals, orbital reliability, ground infrastructure, AI data centers, and very large capital projects.

That makes SpaceX’s execution risk more physical, more regulated, and potentially more binary. If Amazon had delays in fulfillment centers or pricing pressure in retail, the business could still continue operating. If SpaceX faces major delays in Starship, satellite deployment, launch cadence, or orbital AI compute, some of the company’s most important future growth assumptions could be pushed out or reduced.

The Amazon comparison helps explain why investors may tolerate losses during a period of aggressive reinvestment. It does not eliminate the need to ask whether SpaceX’s future profit engines can support the valuation.

Is SpaceX Stock a Good Buy After the IPO?

SpaceX is a remarkable company. It has changed the launch industry, built Starlink into a global satellite-internet platform, and created a long-term roadmap that few companies could realistically attempt.

But the stock already reflects much of that ambition. After a historic IPO, investors are not only paying for what SpaceX has already built. They are also paying for future success in Starship, Starlink expansion, AI infrastructure, space-based computing, and other projects that may take years to fully prove.

That makes the investment case more complicated than the company story. A great business can still become a risky stock if expectations are too high, if execution takes longer than expected, or if future profits do not arrive fast enough to support the valuation.

For investors, the key is not to ignore SpaceX’s achievements. It is to separate the company’s technological success from the stock’s valuation risk. SpaceX may continue to grow into its public-market expectations, but the margin for error is not wide.

The SpaceX story is compelling. The investment case is more complicated.