7 AI Stocks After the Selloff: Which One Has the Strongest Fundamentals?

AI stocks have fallen sharply after a powerful rally, forcing investors to look beyond momentum and ask a more important question: which companies still have the strongest fundamentals when the market turns volatile?

The recent pullback has affected some of the most closely followed names in the AI trade. On June 5, U.S.-traded semiconductor companies lost approximately $1.3 trillion in market value after Broadcom’s results fell short of elevated expectations. NVIDIA, AMD, Micron, and Marvell were among the stocks caught in the selloff. The pressure continued as technology stocks declined further amid concerns about valuations, interest rates, inflation, and geopolitical uncertainty. By June 10, the semiconductor index had fallen approximately 13% over the preceding week.

A falling stock price does not automatically mean a stock has become a bargain. Some AI companies generate rapid revenue growth but remain unprofitable. Others have strong businesses but still trade at valuations that leave little room for disappointment. A smaller share price can attract attention, but it does not necessarily mean that the company is undervalued.

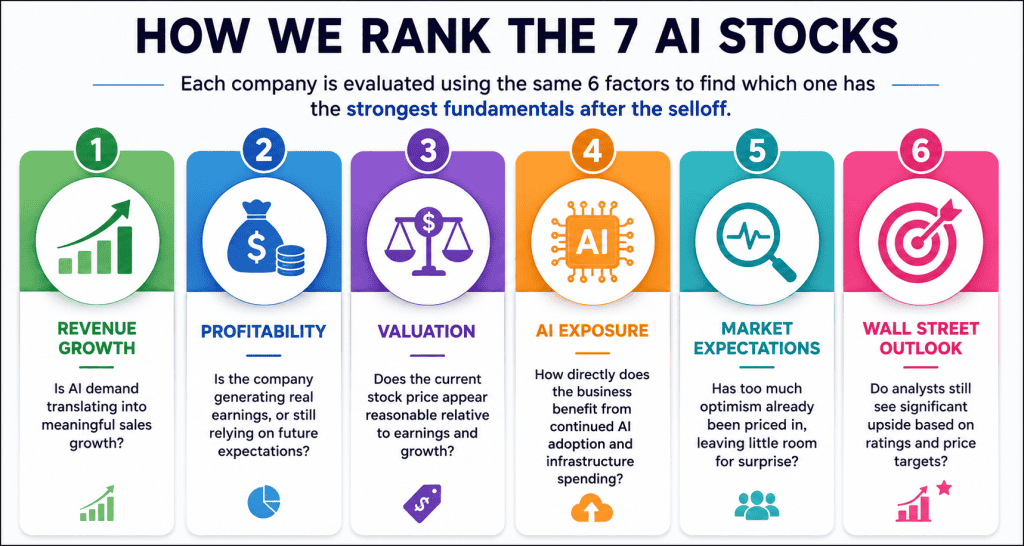

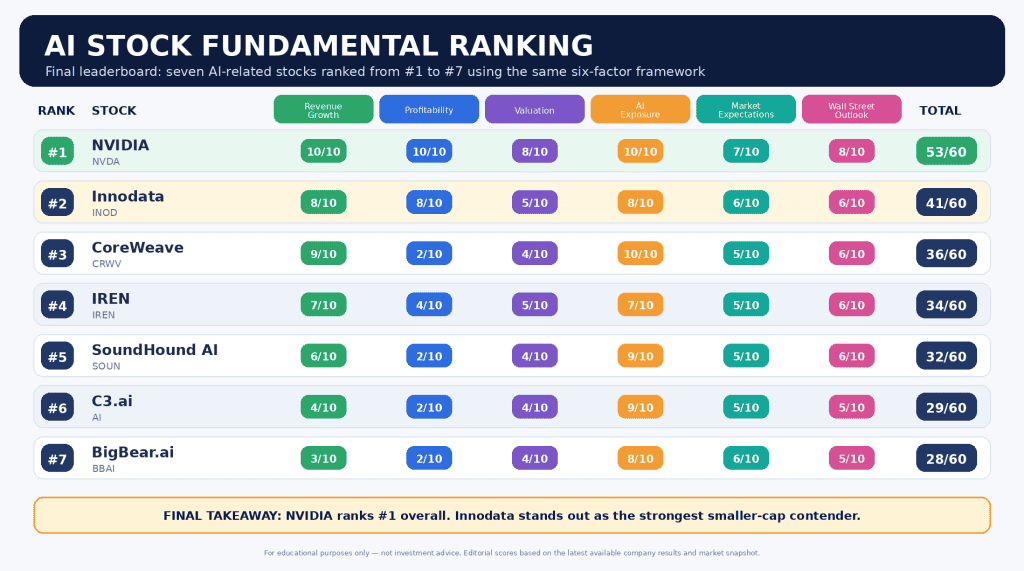

To separate promising businesses from speculative names, this article ranks seven widely followed AI-related stocks from bottom to top. Each company will be evaluated using the same six factors: revenue growth, profitability, valuation, clear exposure to AI demand, market expectations, and Wall Street’s current outlook. The goal is not to predict which stock will rebound first. It is to identify which business currently offers the strongest combination of fundamentals after the selloff.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Always conduct your own research before making investment decisions.

How the 7 AI Stocks Will Be Ranked

This ranking is not based only on which stocks have fallen the most or which shares have the lowest prices. A lower share price may attract attention, but it does not necessarily mean that a company is undervalued. Market capitalization, earnings, growth, and future expectations matter much more when evaluating whether a stock offers a compelling opportunity.

Each of the seven AI-related companies will be reviewed using the same six factors:he stocks will be presented from #7 to #1. The goal is not to identify the stock most likely to bounce first during a volatile week. It is to find the company with the strongest overall combination of business quality, AI exposure, valuation, and future growth potential after the recent selloff.

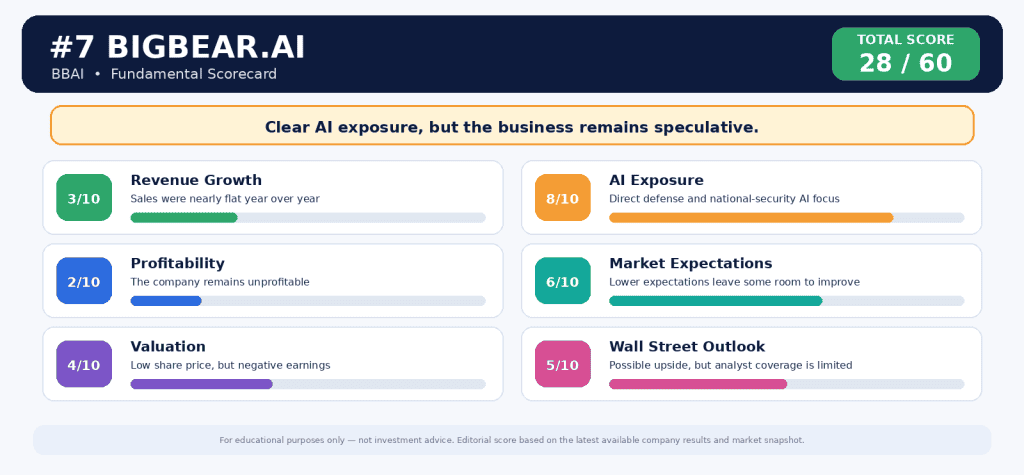

#7 BigBear.ai (BBAI)

BigBear.ai is one of the more recognizable lower-priced AI stocks followed by retail investors. The company focuses on mission-ready artificial intelligence and predictive analytics solutions for national security, defense, intelligence, homeland security, and travel-related customers. Its direct connection to AI makes the story easy to understand: BigBear.ai is trying to help government and commercial organizations make faster decisions in complex operating environments.

The company has reported some encouraging developments. In the first quarter of 2026, backlog increased 14% from the previous quarter to $281.9 million, helped by a $53 million classified national-security award. Gross margin also improved significantly, rising from 21.3% to 34.0% year over year. BigBear.ai affirmed its full-year 2026 revenue guidance of $135 million to $165 million.

However, the financial results still show why BBAI ranks near the bottom of this list. First-quarter revenue was $34.4 million, slightly below the $34.8 million reported during the same quarter a year earlier. The company also reported a net loss of $56.8 million and an adjusted EBITDA loss of $9.9 million.

| Metric | Q1 2026 Result |

|---|---|

| Revenue | $34.4 million |

| Year-over-year revenue growth | -0.9% |

| Gross margin | 34.0% |

| GAAP net loss | ($56.8 million) |

| Adjusted EBITDA | ($9.9 million) |

| Backlog | $281.9 million |

| Full-year 2026 revenue guidance | $135 million to $165 million |

BBAI shares recently traded around $4.02. Publicly reported analyst price targets currently cluster around the $5 to $6 range, suggesting that some analysts still see upside potential. However, analyst coverage remains limited, and the company must convert its backlog into consistent revenue growth before the investment case becomes more compelling.

BigBear.ai deserves attention because its government-focused AI solutions, improving margins, and growing backlog could create a foundation for future growth. But the company has not yet demonstrated consistent revenue expansion or profitability. For now, BBAI remains a speculative AI stock rather than the strongest fundamental opportunity after the selloff.

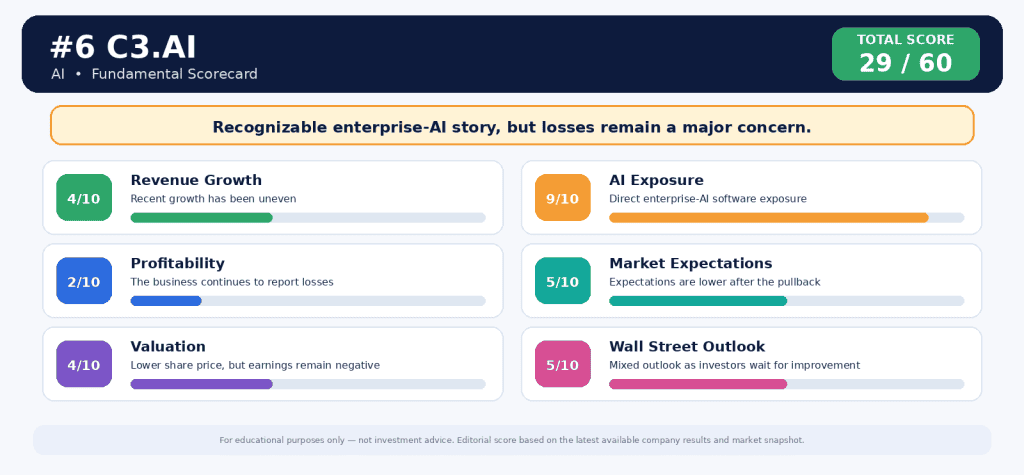

#6 C3.ai (AI)

C3.ai is one of the most recognizable names in enterprise artificial intelligence. The company provides software that helps large organizations develop, deploy, and operate AI applications at scale. Its product portfolio includes the C3 Agentic AI Platform, industry-specific enterprise applications, and generative-AI solutions designed for business use cases.

The company’s direct AI exposure makes the story appealing, but its recent financial performance remains challenging. In the fourth quarter of fiscal 2026, revenue fell 53% year over year to $51.6 million. Subscription revenue accounted for 94% of quarterly sales, showing that the business still has a recurring-revenue foundation. However, C3.ai reported a GAAP net loss of $0.79 per share during the quarter.

For the full fiscal year, revenue reached $250.3 million, while the company reported a GAAP net loss of $3.35 per share. Management acknowledged that recent sales performance was disappointing and said the company has put a restructuring plan in place to focus on revenue growth, cash generation, and non-GAAP profitability.

| Metric | Fiscal Q4 2026 Result |

|---|---|

| Revenue | $51.6 million |

| Year-over-year revenue growth | -53% |

| Subscription revenue | $48.4 million |

| Subscription revenue as a percentage of total revenue | 94% |

| GAAP gross margin | 22% |

| GAAP net loss per share | ($0.79) |

| Cash, cash equivalents, and marketable securities | $575.4 million |

There are a few reasons investors may continue watching the stock. C3.ai ended the quarter with a meaningful cash position, and management expects fiscal 2027 revenue of $210 million to $240 million. The midpoint of that range is above the latest Wall Street consensus estimate reported after earnings. The company is also trying to reduce costs and rebuild its sales organization.

However, C3.ai still has a great deal to prove. Revenue has declined sharply, profitability remains out of reach, and management must show that the restructuring can lead to more consistent sales growth. Recent analyst sentiment also remains cautious. Morgan Stanley reiterated an Underweight rating and a $7 price target following the latest results.

C3.ai earns a higher ranking than BigBear.ai because it has a more established enterprise-software platform, a larger revenue base, and a strong cash position. But the declining revenue and continued losses prevent it from ranking higher. For now, C3.ai remains an interesting enterprise-AI turnaround story rather than one of the strongest fundamental opportunities after the selloff.

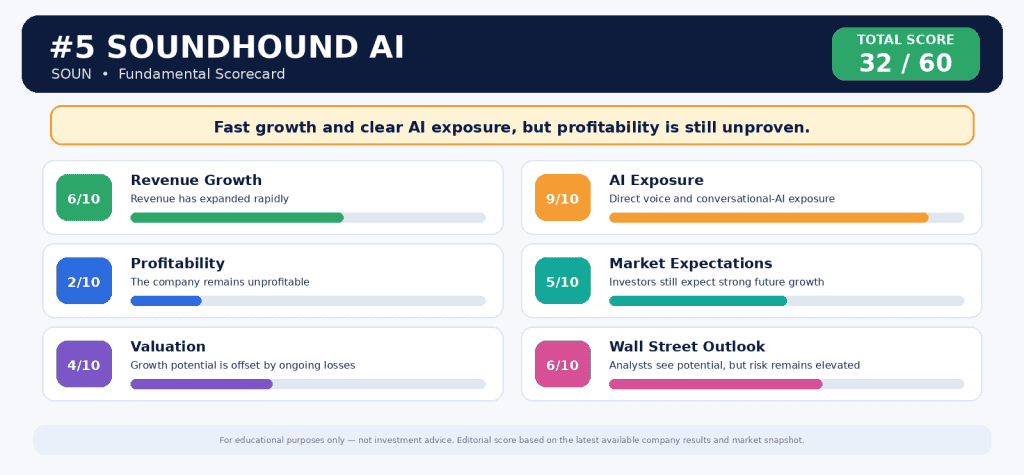

#5 SoundHound AI (SOUN)

SoundHound AI is a voice and agentic-AI company that helps businesses create conversational experiences across phones, drive-thrus, vehicles, smart devices, kiosks, chat systems, and other customer-service channels. Its technology is already used across industries such as automotive, restaurants, financial services, healthcare, retail, and telecommunications.

The company has a clear and easy-to-understand AI story. Rather than competing directly in the expensive race to build chips or data centers, SoundHound focuses on practical AI applications that businesses can use when interacting with customers.

SoundHound reported record first-quarter 2026 revenue of $44.2 million, up 52% from the same period a year earlier. The company said revenue would have increased 88% in its core automotive and IoT AI vertical when excluding the effect of acquisitions. It also reaffirmed full-year 2026 revenue guidance of $225 million to $260 million.

| Metric | Q1 2026 Result |

|---|---|

| Revenue | $44.2 million |

| Year-over-year revenue growth | 52% |

| GAAP gross margin | 31.1% |

| Non-GAAP gross margin | 49.7% |

| GAAP net loss | ($25.0 million) |

| Adjusted EBITDA | ($26.7 million) |

| Cash and cash equivalents | $216 million |

| Debt | None |

| Full-year 2026 revenue guidance | $225 million to $260 million |

SoundHound is also expanding beyond voice assistants. In May, the company launched OASYS, an agentic-AI platform designed to help businesses create, manage, evaluate, and improve AI agents over time. The company has also agreed to acquire LivePerson, a conversational-AI business focused on digital messaging. SoundHound expects the transaction to close during the second half of 2026, subject to customary approvals.

The growth opportunity is attractive, but the financial risks remain significant. Despite the sharp increase in revenue, SoundHound is still losing money. Adjusted EBITDA declined to negative $26.7 million in the latest quarter, and the company used $26.3 million of cash in operating activities. Investors will need to watch whether the company can translate its expanding revenue base into improving margins and a clearer path to profitability.

Wall Street sentiment remains cautiously optimistic. For example, Northland lowered its price target from $14 to $12 after the latest earnings report while maintaining an Outperform rating. The stock recently traded around $6.75, leaving room for potential upside if SoundHound executes successfully. However, published analyst targets should be viewed as sentiment indicators rather than guarantees.

SoundHound ranks above BigBear.ai because its revenue growth is much stronger, its AI use cases are expanding across several industries, and the company ended the quarter with $216 million in cash and no debt. But continued losses and acquisition-related execution risks prevent SOUN from ranking higher. For now, SoundHound remains a promising AI growth story rather than a proven fundamental winner.

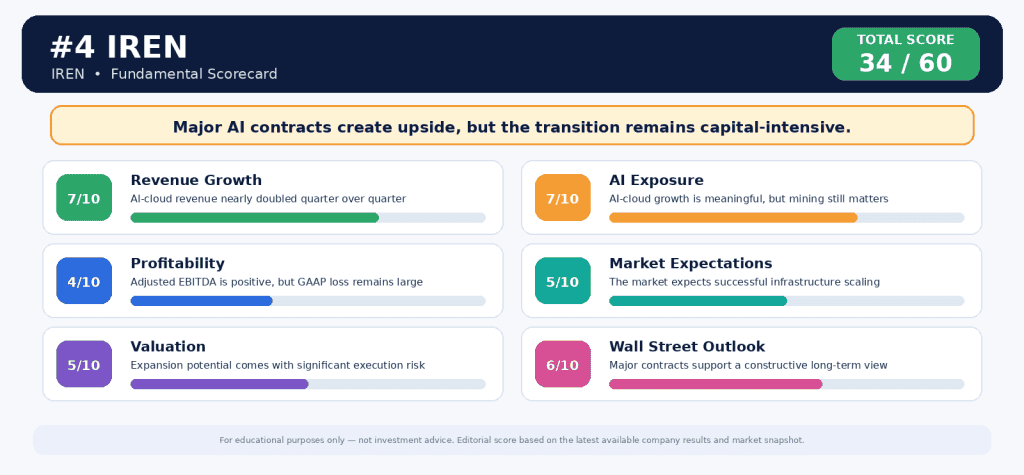

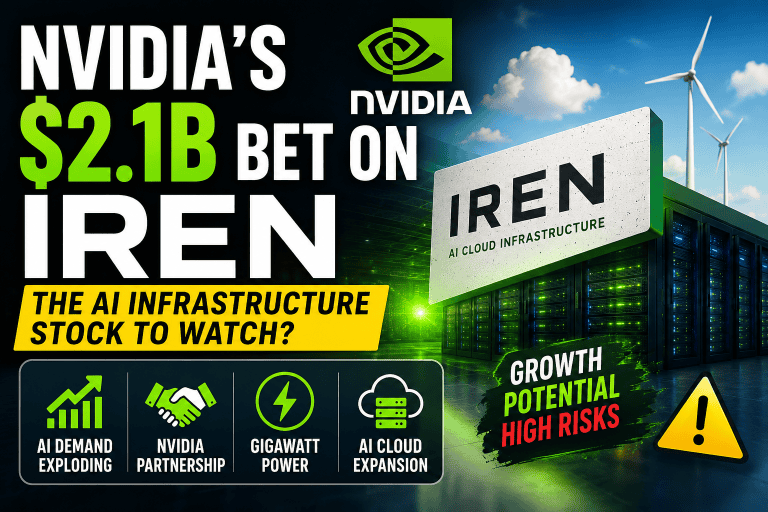

#4 IREN (IREN)

IREN is transitioning from Bitcoin mining into a vertically integrated AI-cloud and data-center company. Its infrastructure includes large-scale data centers and GPU clusters designed for AI training and inference.

The company’s AI opportunity became more significant after announcing a five-year, $3.4 billion AI-cloud contract with NVIDIA and a broader 5GW strategic partnership. IREN is also targeting $3.7 billion in annualized recurring revenue by the end of 2026, although management notes that part of this target depends on successful GPU deployment and utilization.

| Metric | Q3 Fiscal 2026 Result |

|---|---|

| Total revenue | $144.8 million |

| AI-cloud revenue | $33.6 million |

| GAAP net loss | ($247.8 million) |

| Adjusted EBITDA | $59.5 million |

| Cash and cash equivalents | $2.21 billion |

REN ranks above the earlier names because it has major AI contracts, secured power capacity, and a clear path toward scaling its AI-cloud business. However, the transition remains capital-intensive. The company still depends partly on Bitcoin-mining revenue, and investors must watch whether its infrastructure buildout converts into durable AI-cloud revenue.

For now, IREN looks like a promising AI-infrastructure transition story, but not yet a fully proven AI-cloud business.

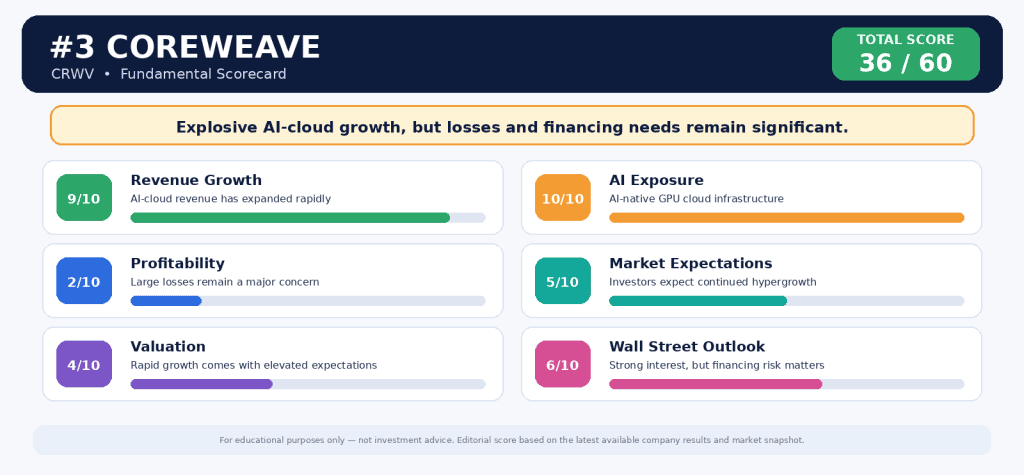

#3 CoreWeave (CRWV)

CoreWeave is an AI-native cloud company that provides GPU infrastructure for demanding artificial-intelligence workloads. Its direct exposure to AI demand is one of the clearest in this ranking.

The company reported first-quarter 2026 revenue of $2.08 billion, more than double the $982 million generated a year earlier. Adjusted EBITDA reached $1.16 billion. However, CoreWeave also reported a GAAP net loss of $740 million, partly reflecting substantial depreciation and interest expenses.

| Metric | Q1 2026 Result |

|---|---|

| Revenue | $2.08 billion |

| Year-over-year revenue growth | 112% |

| Adjusted EBITDA | $1.16 billion |

| GAAP net loss | ($740 million) |

| Net interest expense | ($536 million) |

CoreWeave’s growth potential is significant, but scaling the business requires heavy spending. Reuters reported that the company raised the lower end of its 2026 capital-expenditure outlook to $31 billion while keeping the upper end at $35 billion. The stock fell after earnings because investors were concerned about higher costs and a second-quarter revenue outlook that missed expectations.

Wall Street interest remains strong. Bank of America recently raised its price target to $140 from $120 while maintaining a Buy rating. But the wide gap between rapid revenue growth and substantial losses makes CoreWeave a higher-risk AI infrastructure stock.

CoreWeave ranks #3 because its AI exposure and revenue growth are exceptional. However, financing needs, interest expense, and continued losses prevent it from taking one of the top two positions.

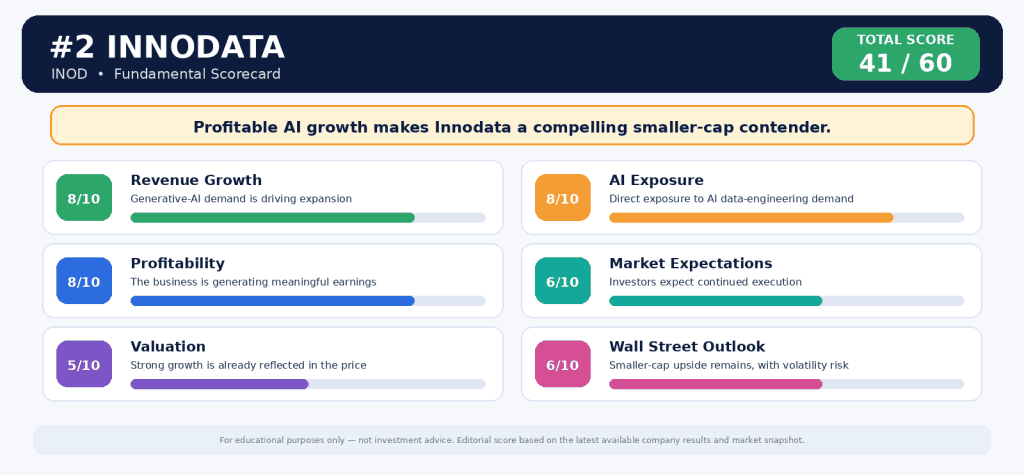

#2 Innodata (INOD)

Innodata provides data-engineering services used to develop and improve generative-AI models, AI agents, and other advanced applications. Unlike several speculative AI stocks in this ranking, Innodata is already generating meaningful profits while continuing to grow rapidly.

In the first quarter of 2026, revenue increased 54% year over year to $90.1 million. Net income nearly doubled to $14.9 million, while adjusted EBITDA rose to $25.0 million. The company also ended the quarter with $117.4 million in cash and short-term investments and no appreciable debt.

| Metric | Q1 2026 Result |

|---|---|

| Revenue | $90.1 million |

| Year-over-year revenue growth | 54% |

| Net income | $14.9 million |

| Adjusted EBITDA | $25.0 million |

| Adjusted EBITDA margin | 28% |

| Cash and short-term investments | $117.4 million |

| Full-year 2026 revenue-growth guidance | Approximately 40% or more |

Management raised its full-year revenue-growth outlook to approximately 40% or more. Innodata also announced new engagements with a major technology company that could generate about $51 million in revenue during 2026, helping diversify its customer base.

Wall Street sentiment has remained positive. Wedbush recently raised its price target from $100 to $120 while maintaining an Outperform rating. However, INOD has already moved sharply, so valuation and customer concentration remain important risks.

Innodata ranks #2 because it combines direct AI exposure with rapid growth, profitability, and a relatively clean balance sheet. It does not match NVIDIA’s scale, but it stands out as one of the strongest smaller AI companies in this comparison.

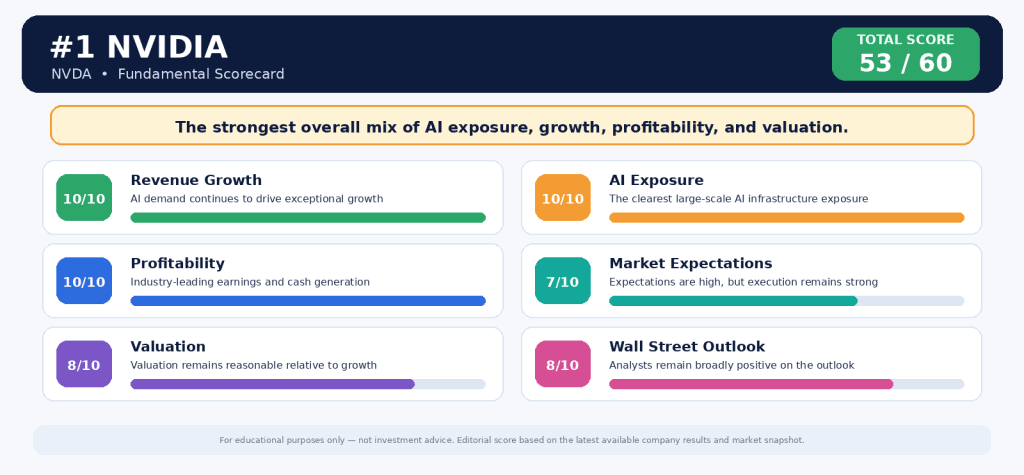

#1 NVIDIA (NVDA)

NVIDIA remains the strongest overall AI stock in this comparison. The company is the clear leader in AI accelerators and data-center systems, giving it direct exposure to the continued buildout of artificial-intelligence infrastructure.

In the first quarter of fiscal 2027, NVIDIA reported record revenue of $81.6 billion, up 85% year over year. Data-center revenue reached $75.2 billion, increasing 92%. The company also guided for approximately $91 billion in second-quarter revenue, ahead of Wall Street expectations.

| Metric | Q1 Fiscal 2027 Result |

|---|---|

| Revenue | $81.6 billion |

| Year-over-year revenue growth | 85% |

| Data-center revenue | $75.2 billion |

| Data-center revenue growth | 92% |

| GAAP gross margin | 74.9% |

| GAAP earnings per diluted share | $2.39 |

| Q2 revenue outlook | Approximately $91 billion |

NVIDIA stands out because it combines exceptional growth with strong profitability. The stock recently traded around $200.42 with a trailing price-to-earnings ratio of approximately 30.5. That valuation is notable because several smaller AI-related companies trade at higher multiples despite having slower growth or weaker earnings.

Wall Street expectations remain high. Publicly available analyst estimates continue to indicate a broadly positive outlook and meaningful potential upside from the recent share price. However, price targets should be viewed as sentiment indicators rather than guarantees. NVIDIA must continue delivering strong results as competition grows and investors look for evidence that AI spending can remain durable beyond the current infrastructure cycle.

NVIDIA ranks #1 because it offers the strongest overall balance of revenue growth, profitability, valuation, direct AI exposure, and market confidence. It may not be the lowest-priced stock in the countdown, but it appears to have the strongest fundamentals after the recent selloff.

Final Takeaway: Which AI Stock Has the Strongest Fundamentals?

After reviewing all seven companies using the same six-factor framework, NVIDIA ranks #1 overall. The company stands out because it combines exceptional revenue growth, strong profitability, direct exposure to AI infrastructure demand, and a valuation that remains reasonable relative to its growth rate.

NVIDIA reported record fiscal Q1 2027 revenue of $81.6 billion, up 85% year over year, while data-center revenue increased 92% to $75.2 billion. That scale and profitability make NVIDIA difficult to match among the companies in this comparison.

Innodata earns the #2 position and stands out as the strongest smaller-cap contender. Its revenue increased 54% year over year in the first quarter of 2026, while adjusted EBITDA reached $25.0 million. The company also raised its full-year revenue-growth outlook to approximately 40% or more.

CoreWeave ranks #3 because its AI-cloud exposure and revenue growth are exceptional. However, the company’s $740 million quarterly net loss and substantial interest expense show why rapid growth does not automatically translate into lower risk.

The remaining stocks still deserve attention, but each carries a more significant tradeoff. IREN has a promising AI-cloud expansion story but remains capital-intensive and still depends partly on Bitcoin-mining revenue. SoundHound AI and C3.ai offer clear AI exposure but have not yet demonstrated consistent profitability. BigBear.ai remains the most speculative name in this ranking because revenue growth is limited and losses remain substantial.

The broader lesson is that a falling stock price does not automatically create a bargain. After a sharp market pullback, the strongest opportunities are often the companies that combine real AI demand with growing revenue, improving earnings, a manageable valuation, and the financial strength to continue investing through market volatility.

Based on those factors, NVIDIA appears to offer the strongest overall fundamentals in this comparison, while Innodata may be worth watching closely for investors interested in a smaller AI-focused growth company.

Great content! Keep up the good work!