Marvell Technology(MRVL) Is Joining the S&P 500: Is This AI Stock the Next Big Winner?

Marvell Technology (MRVL) is attracting fresh investor attention after S&P Dow Jones Indices announced that the semiconductor and data-infrastructure company will join the S&P 500 before the market opens on June 22, 2026. The addition comes after a sharp rally in Marvell shares, fueled by growing excitement around the company’s role in custom AI chips and data-center networking. But with the stock already moving rapidly, investors now face an important question: does joining the S&P 500 create another reason to watch Marvell, or has much of the optimism already been priced in?

Joining the S&P 500 is more than a symbolic milestone. Marvell will replace Pool Corporation as part of the index’s quarterly rebalance. Because the S&P 500 is widely tracked by index funds and exchange-traded funds, the inclusion can introduce Marvell to a much broader group of investors. It also reflects how significantly the company has grown as demand for AI infrastructure continues to expand.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Always conduct your own research before making investment decisions.

Does Joining the S&P 500 Usually Lift a Stock?

Marvell’s immediate rally is consistent with the reaction often seen when a company is selected for the S&P 500. Index-tracking funds may need to adjust their holdings, while inclusion can draw attention from a wider group of investors. However, the stock has already received a significant announcement-related boost. Investors should not assume that another automatic increase will follow when Marvell officially enters the index on June 22.

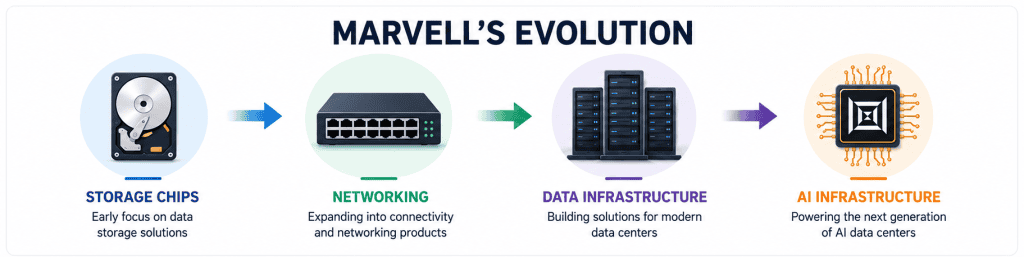

From Storage Chips to AI Infrastructure

Marvell’s story began long before the current AI boom. Founded in 1995 by Sehat Sutardja, Weili Dai, and Pantas Sutardja, the company initially focused on semiconductor technology for data-storage products. Its first product was a specialized read-channel chip for hard drives. Over the years, Marvell expanded beyond storage into networking, connectivity, and broader data-infrastructure solutions.

Today, Marvell is not a household name like NVIDIA, but its technology plays an important role behind the scenes in modern AI data centers. The company develops custom chips and high-speed connectivity products that help large cloud providers move enormous amounts of data efficiently across increasingly complex computing systems. Its portfolio spans custom AI accelerators, processors, optical and copper interconnects, network switches, and storage-related technologies. As hyperscalers build larger AI infrastructure, Marvell is positioning itself as one of the key suppliers enabling those systems to scale.

Why Custom AI Chips Matter

One of the most important parts of Marvell’s AI opportunity is its custom-silicon business. Large cloud providers are no longer relying only on standard, off-the-shelf chips. As AI workloads become larger and more expensive, hyperscalers are increasingly looking for processors designed around their specific performance, power, and cost requirements.

Marvell helps these customers develop custom AI accelerators and other specialized chips for their data centers. These products are not intended to replace every general-purpose GPU. Instead, they allow cloud providers to optimize certain workloads while building AI systems that are more efficient and tailored to their own needs.

Why NVIDIA’s Partnership With Marvell Matters

Marvell’s position in the AI infrastructure market became more significant when NVIDIA announced an expanded strategic partnership with the company through NVLink Fusion. As part of the collaboration, NVIDIA invested $2 billion in Marvell. The two companies are also working together to make it easier for cloud providers to integrate custom chips into NVIDIA-based AI systems.

Under the partnership, Marvell will provide custom XPUs and NVLink Fusion-compatible scale-up networking products. NVIDIA will provide supporting technologies, including CPUs, network-interface cards, data-processing units, NVLink interconnects, and Spectrum-X switches. Together, these components can help customers build semi-custom AI infrastructure while still benefiting from NVIDIA’s broader hardware ecosystem.

The partnership is important because it shows that custom AI chips do not necessarily have to compete directly against NVIDIA’s GPUs. In many cases, specialized processors can work alongside NVIDIA technology inside the same data center. For Marvell, this creates an opportunity to participate in the growth of AI infrastructure even as NVIDIA remains the dominant name in accelerated computing.

Marvell’s Financial Performance: AI Demand Is Driving Revenue Growth

Marvell’s expanding role in AI infrastructure is beginning to show up clearly in its financial performance. After generating relatively modest revenue growth in fiscal 2025, the company reported a much stronger fiscal 2026 as demand from its data-center customers accelerated. Revenue increased by more than 42% year over year, reaching a record $8.19 billion.

The improvement is significant because Marvell had reported net losses in each of the previous two fiscal years. In fiscal 2026, the company returned to profitability and reported diluted earnings of $3.07 per share. However, investors should interpret the sharp increase in net income carefully. The result was helped by a large gain from the sale of Marvell’s automotive Ethernet business, meaning the headline profit figure does not come entirely from recurring operations.

| Fiscal Year | Revenue | GAAP Net Income (Loss) | GAAP Diluted EPS |

|---|---|---|---|

| Fiscal 2026 | $8.19 billion | $2.67 billion | $3.07 |

| Fiscal 2025 | $5.77 billion | ($885.0 million) | ($1.02) |

| Fiscal 2024 | $5.51 billion | ($933.4 million) | ($1.08) |

Note: Marvell’s fiscal 2026 ended on January 31, 2026. Fiscal 2025 ended on February 1, 2025, and fiscal 2024 ended on February 3, 2024.

The revenue trend may be more informative than the headline net-income figure. Marvell said fiscal 2026 revenue growth was driven primarily by strength in its data-center business, which continues to benefit from AI-related demand.

That momentum has continued into fiscal 2027. In the first quarter, Marvell reported record revenue of $2.42 billion, up 28% year over year. Management guided for approximately $2.70 billion in second-quarter revenue, which would represent growth of about 35% at the midpoint. The company also expects revenue growth to continue accelerating during fiscal 2027, supported by continued strength in its data-center business.

Marvell’s Long-Term AI Growth Opportunity

Marvell’s recent growth is encouraging, but the larger investor question is whether the company can continue expanding as AI data centers become more complex. Management believes the opportunity extends well beyond the current wave of infrastructure spending. Marvell has raised its fiscal 2028 revenue outlook to approximately $16.5 billion and expects its custom-chip business alone to exceed $10 billion in annual revenue by fiscal 2029.

The custom-silicon opportunity is only one part of the story. As AI models grow larger, data centers must connect thousands of processors and move enormous volumes of information quickly and efficiently. Marvell supplies many of the technologies needed to support this expansion, including high-speed interconnects, optical solutions, and network switches. This gives the company multiple ways to benefit as cloud providers invest in larger and more advanced AI systems.

The long-term outlook is promising, but it also sets a high bar. Marvell will need to convert its custom-chip programs into sustained revenue growth while continuing to compete in a rapidly evolving semiconductor market. Investors should view the company’s fiscal 2028 and fiscal 2029 targets as an indication of the potential opportunity rather than a guaranteed outcome.

What Wall Street Expects After Marvell’s Sharp Rally

Marvell’s long-term AI opportunity has attracted growing interest from Wall Street. Following the company’s latest earnings report and stronger long-term outlook, several analysts raised their price targets as expectations increased for Marvell’s custom-chip and data-center businesses.

| Analyst Firm | Rating | Previous Price Target | Updated Price Target |

|---|---|---|---|

| Deutsche Bank | Buy | $120 | $240 |

| BofA Securities | Buy | $200 | $240 |

| Barclays | Overweight | $150 | $275 |

These increases show that analysts have become more optimistic about Marvell’s growth prospects. However, the stock has moved even faster than many of the revised estimates. Marvell shares closed at $288.85 on June 8, 2026, after rising more than 9% following the S&P 500 announcement. Reuters reported that the stock had gained approximately 59% since May 27 and had more than tripled in value as investor enthusiasm around AI infrastructure intensified.

The sharp rally creates an important distinction between confidence in Marvell’s business and expectations for its stock price. Wall Street analysts may remain positive about the company’s longer-term prospects, but the stock is already trading above several recently increased price targets.

This does not necessarily mean that Marvell’s rally is over. Price targets can lag behind fast-moving developments, and analysts may revise their estimates again as the company reports additional results. Still, the recent price action suggests that investors are already pricing in a significant amount of future growth.

For new investors, the question is no longer simply whether Marvell can benefit from AI infrastructure spending. The more difficult question is whether the company can deliver results strong enough to support the expectations already reflected in its share price.

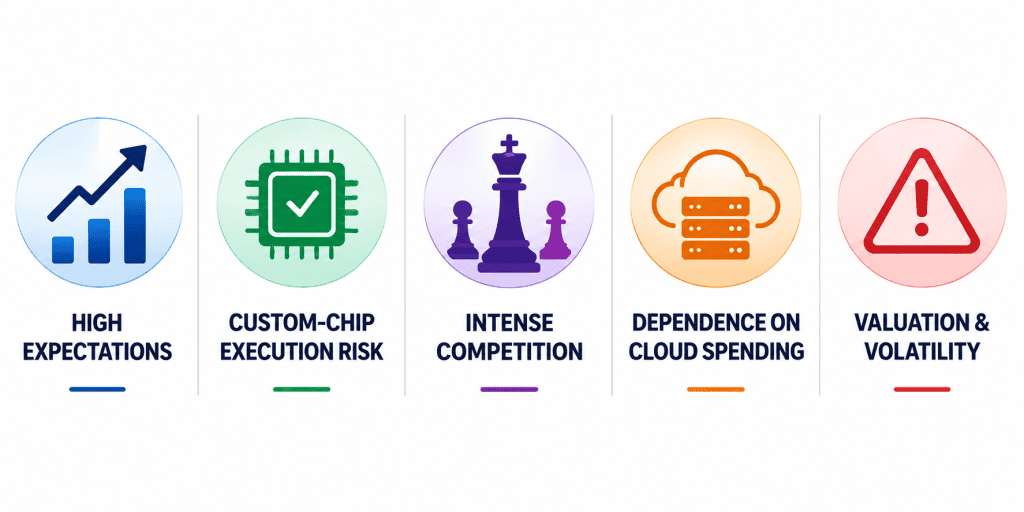

Risks Investors Should Consider

Marvell’s AI opportunity is significant, but the company still faces several challenges that investors should not overlook. After such a sharp rally, expectations are high. Marvell must continue converting its custom-chip opportunities into meaningful revenue while maintaining its position in a highly competitive and fast-moving semiconductor market.

Execution is one of the most important risks. Marvell’s custom-chip growth depends on winning major design programs and successfully moving those products into volume production. Delays, weaker-than-expected customer demand, or difficulty meeting the rapid pace of innovation required by large customers could affect future growth.

The company is also increasingly tied to AI data-center spending. This creates a major opportunity while demand remains strong, but it can also expose Marvell to changes in cloud-infrastructure budgets. A slowdown in spending by hyperscalers or delays in large data-center projects could place pressure on results.

Competition remains another important factor. Marvell operates across custom silicon, networking, and connectivity markets where customers have several alternatives. The company must continue investing in new products and maintaining strong customer relationships to defend its position.

Finally, valuation and volatility should not be ignored. Marvell may continue benefiting from the expansion of AI infrastructure, but the stock’s rapid rise leaves less room for disappointment. Investors should watch whether revenue growth, custom-chip execution, and data-center demand remain strong enough to support the expectations already reflected in the share price.

Final Takeaway: Is Marvell Worth Watching After Its S&P 500 Addition?

Marvell’s addition to the S&P 500 has brought the company to the attention of a much broader investor audience. But the index inclusion is only a starting point. The more important story is Marvell’s growing role in the infrastructure behind modern AI data centers.

The company is positioned across several important areas, including custom silicon, high-speed interconnects, and network-switch products. Marvell describes itself as a critical AI-infrastructure partner for hyperscalers building increasingly complex systems.

The opportunity is significant, but expectations are already high after the stock’s sharp rally. For investors considering MRVL, the key question is no longer whether the company can benefit from AI spending. It is whether Marvell can deliver results strong enough to justify the optimism already reflected in its share price.