Cohesity IPO Strategy: Why AI Data Management Is the Next Big Software Trade

The AI investment story is moving deeper into the stack, and most investors haven’t caught up yet.

The first wave was obvious—chips, GPUs, and cloud infrastructure. The second wave followed naturally data centers, power, and networking. But as enterprises begin deploying AI at scale, a more fundamental constraint is emerging: not compute, but data. Specifically, how enterprise data is stored, secured, accessed, and made usable for AI systems.

That shift is pulling an underappreciated category into focus enterprise data management. And at the center of that shift is Cohesity, a company preparing for a potential IPO that may say more about the future of enterprise software than most AI names currently dominating headlines.

This is not just another IPO story. It is a test of whether the market is ready to value data platforms as core AI infrastructure.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Always conduct your own research before making investment decisions.

A Company Built Ahead of Its Time

Cohesity was founded in 2013 by Mohit Aron, who previously co-founded Nutanix—a company that helped redefine enterprise infrastructure through hyperconverged systems. That lineage matters, because Cohesity follows a similar philosophy: simplify fragmented enterprise systems into a unified platform.

For years, that idea lived in what many investors would have considered a low-excitement category—backup and data protection. But the rise of AI has fundamentally changed the importance of that layer. Data is no longer passive. It is now the raw material for intelligence, automation, and decision-making.

Cohesity’s platform consolidates backup, recovery, security, and data orchestration into a single system. More importantly, it positions itself as a control layer that enables enterprises to actually use their data for AI. In an environment where data is fragmented across hybrid and multi-cloud systems, that positioning is no longer optional—it is becoming essential.

The IPO Strategy: Scale First, Then Story

Cohesity didn’t delay its IPO because of timing alone—it delayed it because it wasn’t in the right position to go public. The company had already filed confidentially in 2021, but instead of moving forward, management chose to pause the process and pursue a much larger objective: acquiring the enterprise data protection business of Veritas Technologies. That decision effectively reset the IPO timeline.

The Veritas deal, completed in December 2024, was not about incremental growth. It was about changing Cohesity’s standing in the market. Before the acquisition, Cohesity was one of several vendors in a fragmented data protection space. After the deal, it became the largest player globally, with roughly 19% market share and a significantly expanded enterprise footprint.

In practical terms, the company moved from a mid-tier competitor to a scale player with over $1.5 billion in annual recurring revenue and more than 12,000 enterprise customers. That shift matters because public market investors don’t price “potential leaders”—they price companies that already look like one.

Management has been explicit about this internally. The IPO wasn’t treated as the goal—it was treated as a milestone that only makes sense after scale, revenue, and market position are in place. So the sequence was reversed:

Cohesity chose scale → then IPO

Instead of IPO → then scale,

Valuation Expectations and Market Framing

Cohesity’s valuation going into a potential 2026 IPO is not arbitrary, it is being shaped by a combination of its current scale, recent consolidation, and private market signals.

Following its merger with the enterprise data protection business of Veritas Technologies, the combined entity reached approximately $1.5 billion in annual recurring revenue (ARR) . This places Cohesity in a different category than most pre-IPO software companies. it is already operating at a scale where public market comparability becomes relevant.

At the same time, the company’s last major funding round in late 2024 valued it at roughly $7 billion post-money . More recent secondary market activity suggests implied share prices in the range of ~$15–$17 per share, indicating that private market expectations have remained relatively stable since the merger.

However, Cohesity’s IPO ambitions appear to go beyond that baseline. Management has signaled an intention to target a valuation closer to the upper end of the category potentially in the $15B–$17B range . That implies a significant step-up from its last private valuation.

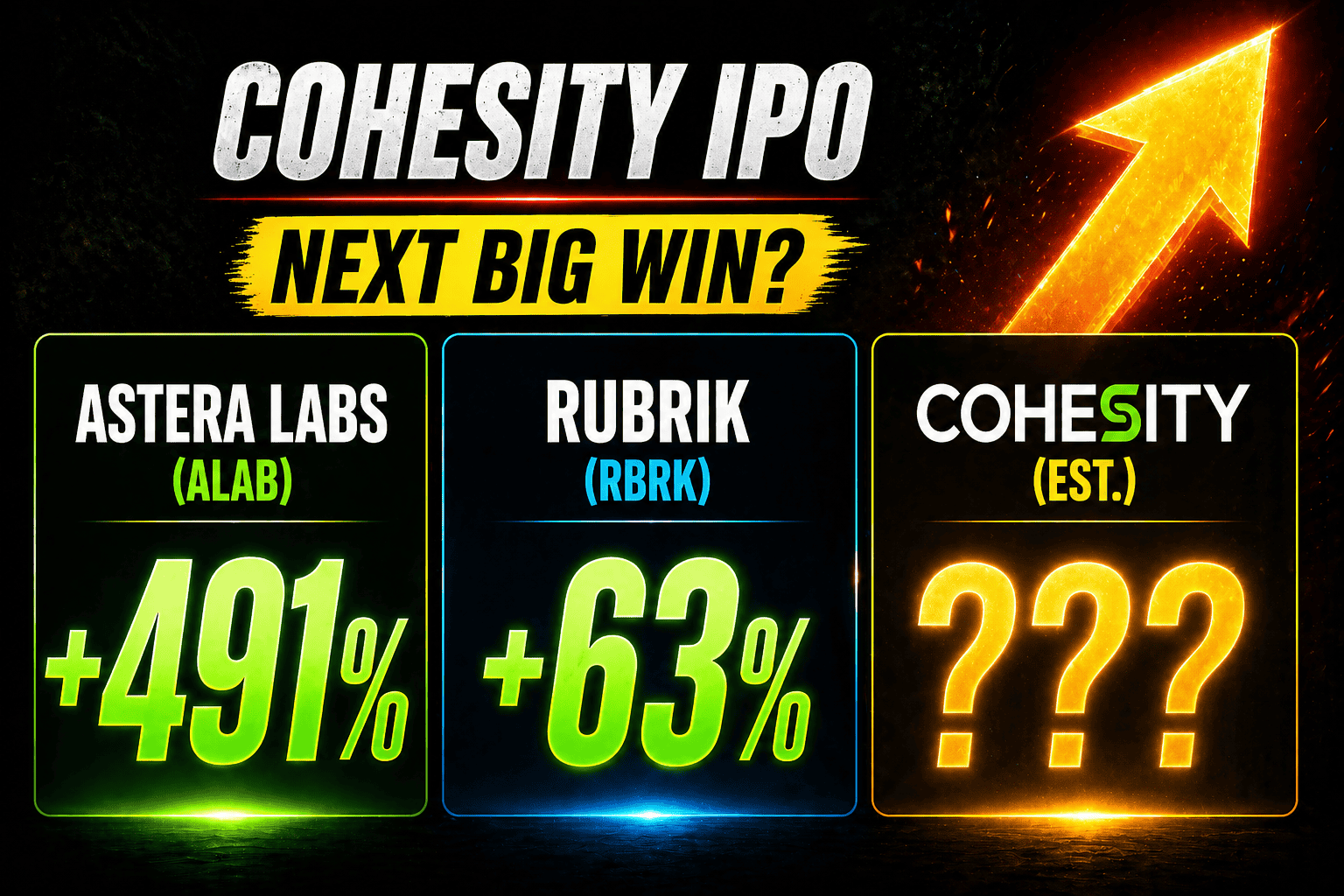

What we know from Previous IPOs

The upcoming Cohesity IPO is widely considered the final “Big Tech” listing of the 2026 season. As of April 2026, the company has transitioned from a data storage provider to an AI Security powerhouse, largely fueled by its merger with Veritas. For investors on aistockshub.com, the critical question is whether Cohesity will follow the explosive path of hardware connectivity plays or the steady, resilient climb of its direct data-security peers.

The table below tracks how similar data-driven companies have performed from their debut day through their first year of trading, providing a roadmap for what we might expect from Cohesity.

Data-Centric IPO Performance Comparison (2023–2026)

| Company (Ticker) | Sector | Current Price (Apr 24, ’26) | IPO Price | % Since IPO | 1-Day Debut Price | 1st Week Perf. | 1st Year Perf. |

| Astera Labs (ALAB) | AI Connectivity | $212.84 | $36.00 | +491% | $62.03 (+72%) | +122% | +92% |

| Rubrik (RBRK) | Data Security | $52.28 | $32.00 | +63% | $37.00 (+15%) | +6% | +118% |

| Tempus AI (TEM) | Health Data/AI | $52.12 | $37.00 | +41% | $40.25 (+9%) | -23% | +93% |

| Klaviyo (KVYO) | Marketing SaaS | $19.45 | $30.00 | -35% | $32.70 (+9%) | +17% | +14% |

| Cohesity (Est.) | AI Data Mgmt. | $22.60* | ~$24.00 | N/A | TBD (Late ’26) | TBD | TBD |

IPO Market Performance Analysis

The broader landscape for AI-related IPOs has been defined by a clear split between “Essential Infrastructure” and “Marketing SaaS.” Companies like Astera Labs and Tempus AI demonstrate the high-volatility, high-reward nature of this sector; while Astera has become a massive winner (up over 490%), it required investors to hold through significant post-IPO swings.

Conversely, Klaviyo highlights the risks of the “SaaS fatigue” trend, currently trading 35% below its IPO price as investors shift capital away from marketing tools and toward the core data layers that actually power AI models. For your audience, the takeaway is clear: 2026 investors are rewarding companies that provide the “picks and shovels” (connectivity and data processing) rather than those just using AI for customer acquisition.

The Sector Rival: Rubrik (RBRK)

Because Rubrik operates in the exact same “Cyber-Resilience” sector as Cohesity, it serves as the ultimate “North Star” for this IPO. Rubrik’s performance shows a “slow-burn” success model: it didn’t have a massive 100% pop on Day 1, but its 1st Year Performance (+118%) was exceptional as enterprises realized that data backup is the only true defense against AI-driven ransomware.

Cohesity is currently positioned to be the “Value” play in this rivalry. While Rubrik is the high-growth specialist, Cohesity’s merger with Veritas has given it a 19% market share, making it the “incumbent” giant. If Cohesity prices near the $24 mark, it will be entering at a more attractive multiple than Rubrik did, offering a potential “catch-up” trade for investors who missed the Rubrik rally.

The NVIDIA Signal: Why It Matters

If the Veritas merger gave Cohesity scale, its alignment with NVIDIA gives it relevance in the AI conversation. In 2026, Cohesity was named a launch partner for NVIDIA’s inference microservices. The real significance isn’t the partnership itself, it’s the architecture behind it.

Enterprises don’t want to move sensitive data into external systems just to run AI. It’s slow, expensive, and risky. Cohesity’s approach flips that: bring AI models to where the data already lives. If that model gains traction, it solves a real bottleneck in enterprise AI. But partnerships alone don’t guarantee adoption, the value will depend on how widely customers actually use it.

Gaia and the RAG Layer

Cohesity’s Gaia platform is an attempt to turn backup data into something useful. Instead of sitting idle, historical data including emails, documents, code. can be indexed and queried using AI through a retrieval-augmented generation (RAG) approach. In simple terms, it lets companies ask questions and get answers grounded in their own data.

If it works, backup shifts from being insurance to something closer to a knowledge system. The challenge is execution. Many vendors are building similar capabilities. The difference will come down to how well this integrates into real workflows not just whether the feature exists.

Where the Story Can Break

The biggest risk is integration. Cohesity now has to combine a cloud-native platform with Veritas’ legacy enterprise systems. That’s not just a technical problem, it affects product direction, sales execution, and growth consistency.

There’s also the financial side. Large acquisitions often bring debt, and in a higher-rate environment, that can limit flexibility. Finally, competition from Amazon Web Services and Microsoft Azure isn’t going away. Cohesity’s advantage is being platform-neutral, but that also means competing with the infrastructure providers themselves.

The Final Verdict: Is Cohesity a Day 1 Buy?

Cohesity will likely see strong interest at IPO, but that does not automatically make it a Day 1 opportunity. The company already has scale and market share, so much of the story may be reflected in the pricing. The key question is whether the market views it as a traditional data protection vendor or as part of the AI data infrastructure layer.

If pricing is reasonable, early entry could make sense. If the stock opens with a strong premium, waiting for post-IPO clarity may be the better approach. In the end, the real opportunity is unlikely to be defined on Day 1. It will depend on how Cohesity executes and how the market values its role in the AI stack over time.